Oma Säästöpankki Oyj: The Power That Elects Itself

An article on the concentration of power, conflicts of interest, and the structure that made the crisis possible at Oma Säästöpankki

When documents vanish from the vault

During our phone call on 10 November 2025 (which you can listen to here), it emerged that a significant number of credit decision documents have disappeared from the vaults of Oma Säästöpankki's Seinäjoki branch — documents that absolutely should have been preserved. These are not just any papers. They are the records that document the basis for granting loans: collateral, risk assessments, decision-makers.

Freely quoting the call: "Things have disappeared that should not be possible to lose. Documents are gone that the bank is absolutely required to retain."

This raises a fundamental question: Who has access to the bank's vault?

Generally speaking, access to bank archives and vaults is extremely restricted. It typically requires a senior position within the organisation, special authorisation, or the simultaneous presence of multiple individuals. Credit decision documents are core bank documentation: their disappearance is not an "accident" but either a serious system failure or a deliberate act.

If documents have been systematically destroyed, it means that one or more individuals in senior positions made a decision to destroy them. If this happened while the bank was already under investigation by the National Bureau of Investigation (KRP) and the Financial Supervisory Authority (Finanssivalvonta), we are dealing with something exceptionally serious and brazen.

The disappearance of documents is merely a symptom: The real question is: what kind of organisational structure allowed a situation where this could happen?

1. The paradox of foundation ownership: Ownerless money that has masters

Oma Säästöpankki's ownership structure is exceptional in the Finnish listed company landscape. Approximately 75 per cent of the shares belong to non-profit savings bank foundations and cooperatives. The largest owner is Etelä-Karjalan Säästöpankkisäätiö (South Karelia Savings Bank Foundation), with roughly a 25–30 per cent stake (verified 17 December 2025).

Finnish foundation law creates a unique structure: a foundation has no actual owners in a legal sense. According to the Finnish Patent and Registration Office, the persons registered as board and supervisory board members in the foundation register are considered the foundation's beneficial owners — but these individuals own nothing. They merely administer.

In practice, this means:

- First, no one bears legal responsibility for the foundation's assets in the same way as in a limited company.

- Second, foundations are not required to separately declare beneficial owners in the trade register.

- Third, it creates "ownerless money": wealth that no one owns but someone controls.

The historical structure of savings bank foundations is telling. One commentator described it as follows: "Elections would produce 10 new members for the 40-person representative body. Then these old 40 and new 10 would convene and choose 40 'new' representatives from among themselves. Usually the old 40 continued."

The structure enables a closed circle in which the same people elect one another.

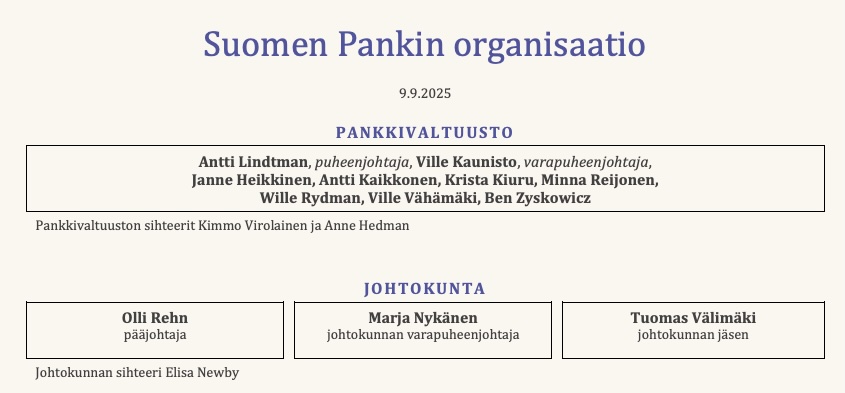

2. The nomination committee: Seven years of the same faces

OmaSp's shareholders' nomination committee was established in connection with the stock exchange listing in November 2018. The committee prepares proposals for board members, board size, and remuneration — in practice, it decides who runs the bank.

Nomination committee composition as of 1 June 2025:

| Member | Foundation | Role |

|---|---|---|

| Raimo Härmä (chair) | Etelä-Karjalan Säästöpankkisäätiö | Largest owner, approx. 25% |

| Ari Lamminmäki | Parkanon Säästöpankkisäätiö | 2nd largest, approx. 10% |

| Jouni Niuro | Liedon Säästöpankkisäätiö | 3rd largest |

| Aino Lamminmäki | Töysän Säästöpankkisäätiö | 4th largest, approx. 5% |

| Simo Haarajärvi | Kuortaneen Säästöpankkisäätiö | 5th largest |

A little-known fact: Ari and Aino Lamminmäki have sat on the nomination committee continuously since its founding — now for a full seven years.

No public source directly confirms their family relationship, but circumstantial evidence strongly suggests marriage: the Ylä-Satakunta newspaper reported in June 2023 on the sale of Ari Lamminmäki's bus company: "Ari Lamminmäki will continue as the person responsible for the company's transport operations and as an adviser and board member, and Aino Lamminmäki in the company's sales and marketing."

Their relationship — in all likelihood a marriage — has never been publicly reported in OmaSp's Corporate Governance documents.

What does the Lamminmäki couple control?

Of ownership, approximately 14–16 per cent (shares worth roughly 50 million euros combined). Of nomination committee voting power, 40 per cent (2 out of 5 seats).

It was only at the 2025 annual general meeting that a conflict-of-interest clause was added to the nomination committee's rules of procedure: "A nomination committee member shall not participate in the handling of a matter concerning themselves or a close relative." This suggests the problem was recognised — but only after the crisis, behind closed doors.

3. Jyrki Mäkynen's triple role: Bank, central bank, business lobby

Jyrki Mäkynen (b. 1964) is the most complex figure in this case, owing to his numerous overlapping roles.

At OmaSp, Mäkynen served as chairman of the board from 2009 to 2014 and deputy chairman from 2014 to 2024 — a total of 15 years at the heart of the bank's governance. OmaSp itself stated that Mäkynen "is not independent in relation to the company" due to his long board tenure.

Simultaneously, Mäkynen served as chairman of Suomen Yrittäjät (Federation of Finnish Enterprises) from 2014 to 2020, during which time he represented over 100,000 Finnish entrepreneurs, many of whom are clients of the bank.

And most critically: in 2014, Mäkynen was appointed as a member of the Bank of Finland's Payment Council. The Payment Council is a body operating in conjunction with the Bank of Finland that brings together payment service users, providers, and authorities to develop retail payments. It analyses changes in the operating environment and the effects of regulation — that is, matters that directly concern banks like OmaSp.

Finanssivalvonta, led by Director General Tero Kurenmaa, also operates in conjunction with the Bank of Finland.

Mäkynen thus sat simultaneously on:

- The bank's board, which made lending decisions.

- A central bank body that deals with banking regulation.

- The leadership of a business lobby that advocates to the bank on behalf of its clients.

OmaSp is notably a bank favoured by small entrepreneurs — the very segment from which the bank aggressively pursued its greatest growth.

This triple role constitutes a structural conflict of interest in which the same individual influences decision-making at multiple levels simultaneously.

Mäkynen resigned from OmaSp's board on 5 November 2024. In late 2025, he was charged with misuse of insider information together with two other board members.

4. A dismissed CEO still manages the owner's money

Pasi Sydänlammi led Oma Säästöpankki for 15 years: from September 2009 to June 2024. He was dismissed on 19 June 2024 when the bank published the results of an internal review into lending practices that violated the bank's own guidelines.

The annual general meeting did not grant Sydänlammi a discharge from liability. The bank contested his severance package of over 2 million euros in arbitration proceedings.

Yet Sydänlammi did not leave OmaSp's orbit.

He continues to serve as the agent of Töysän Säästöpankkisäätiö — a foundation that is one of the bank's largest owners. Sydänlammi is responsible for the foundation's investment activities, including its significant OmaSp holding.

Ilkka-Pohjalainen ran the headline in December 2024: "Dismissed from the bank, Pasi Sydänlammi still manages OmaSp's major owner's money."

The situation is structurally absurd: a dismissed CEO, denied discharge from liability, still manages investments for a foundation that is a major bank owner — and whose chair (Aino Lamminmäki) sits on the nomination committee deciding the composition of the board.

Similarly, former deputy CEO Pasi Turtio served as CEO of Kuortaneen Säästöpankkisäätiö alongside his work at OmaSp before his departure. The bank's management thus carried out duties for the owner foundations on the side, completely blurring the line between owners and executive management.

5. Raimo Härmä: The voice of the largest owner

Raimo Härmä leads Etelä-Karjalan Säästöpankkisäätiö, OmaSp's largest owner. He has served as chair of the nomination committee since its establishment in 2018.

Härmä's other roles:

- He serves on the board of S-Pankki, a competing bank (which, according to rumours, would absorb the personal banking clients if the bank were to collapse).

- He is chairman of the board of Haminan Energia Oy.

- He is a Boardman partner*, meaning he holds membership in one of Finland's most influential networks of professional board directors.

Härmä led swift board changes in the name of the major owners in the midst of the crisis, commenting: "Banking is a trust business."

Etelä-Karjalan Säästöpankkisäätiö is domiciled in Lappeenranta, right near the Russian border. The foundation was established in its current form in 2014, and its public financial records have not been available for the last five years.

The Boardman network also includes numerous members who have been business partners with Pasi Turtio and Antti Korpela in joint ventures such as X-Flite Oy and New House Innovation Oy, as well as the Lauttasaaren Onni housing project and other ventures.

6. The FinCap network: Subsidiary boards intertwined

We have previously reported on Pasi Turtio's questionable business dealings, which you can read about here.

OmaSp's crisis is equally closely linked to the Seinäjoki-based FinCap group, owned by Janne Kotamäki (50%) and Raimo Sarajärvi (30%). OmaSp holds significant ownership stakes and loans within the FinCap network:

City Kauppapaikat Oy: OmaSp owns 42.7% (balance sheet value 17.8 million euros). Sarajärvi serves as CEO. Pasi Sydänlammi sat on the board.

GT Invest Oy: OmaSp owns 43.3% (balance sheet value 6.7 million euros). Sarajärvi serves as chairman of the board. Pasi Sydänlammi sat on the board.

FinCap Asunnot Oy: Sydänlammi served as a board member.

The structure means the bank's CEO sat on the same boards as a property investor whose companies the bank granted loans to. According to Talouselämä, Sydänlammi and deputy CEO Turtio also made personal co-investments with Sarajärvi and Kotamäki, including in an apartment development project in Lauttasaari, which Talouselämä has reported on extensively.

OmaSp holds corporate mortgages and guarantees in FinCap companies totalling over 38 million euros. In 2024, several FinCap companies reported loss of share capital.

7. Who has access to the vault?

Let us return to what we consider the most important question: Who has access to the bank's vault?

Typically, access to bank archives and vaults is restricted to the following:

CEO and deputy CEO: the highest level of operational management.

Chief Risk Officer and Compliance Officer: supervisory functions.

Archivist or documentation manager: operational responsibility.

Auditors: periodically during audits.

Authorities: Finanssivalvonta, police with a specific order.

Credit decision documents are core bank documentation. Their systematic disappearance requires:

First, access to the archive, either physically or digitally.

Second, knowledge of which documents to destroy.

Third, the ability to act without oversight.

If documents were destroyed while the bank was already under investigation — or conveniently just before — the perpetrator must have held a senior position, or multiple individuals must have acted in concert.

This raises a broader question: What kind of organisational culture allows a situation where critical documents can vanish? The answer lies in the power structure described above: when the same people elect one another, oversee one another, and benefit from one another, genuine external control is absent — and when you add the entire OmaSp staff's personal shareholdings in OmaSp, the result is what we are now reading about in the press.

8. Employee ownership: The entire organisation is tied to the share price

Employee share ownership at Oma Säästöpankki is exceptionally widespread for the Finnish banking sector. Following the IPO in December 2018, over 60 per cent of staff owned shares in the company — a fact confirmed by then-CEO Pasi Sydänlammi in a stock exchange release.

The employee offering was so oversubscribed that supply had to be increased by 42 per cent from the original. Employees were able to subscribe for shares at a 10 per cent discount, with the average subscription being nearly 5,000 euros per participant. At the time, the bank employed approximately 270 people.

From 2024 onwards, OmaSp has expanded employee share ownership through its OmaOsake programme, in which around 600 people now participate. In addition, approximately 45 key personnel, including the CEO and the management team, belong to a separate share-based incentive scheme. The CEO is required to hold shares worth at least their gross annual salary.

This creates a deep structural conflict of interest.

When a significant proportion of staff own shares in their employer, every report of misconduct is a potentially self-harming financial act. An employee whose savings are tied up in the bank's share price faces a calculation: do I report suspicious activity if it could crash the share price and put my own investments at risk?

The situation is particularly sensitive in banking, where maintaining trust is critical. A single negative news story can trigger a bank run or a share price collapse. The staff know this.

Deferred bonus payments — distributed in five instalments over four years — and shareholding requirements further strengthen this financial bond. An employee cannot simply sell their shares and speak freely; they are bound to the system for years ahead.

This explains one of the central riddles of the crisis: Why did no one report problems earlier? Why were zero reports filed through the whistleblowing channel? Why could documents vanish without raising internal alarms?

The answer is structural: the entire organisation was — and remains — bound to silence through financial incentives.

9. Finanssivalvonta warned in 2022 — nothing was done

As early as December 2022, Finanssivalvonta recommended that OmaSp ensure its board had sufficient financial sector experience and the ability to understand industry-related risks. This warning did not lead to adequate action before the crisis erupted.

The bank had no separate audit committee before the summer of 2024 — instead, the "mates' club" board handled these duties itself. No reports were filed through the whistleblowing channel, and we now understand better why: internal control structures were either deficient or effectively non-existent.

In April 2025, Finanssivalvonta's inspection report revealed "fundamental problems" in customer due diligence and anti-money laundering. OmaSp has set aside a 3-million-euro provision for potential sanctions.

Conclusions: A structure that oversees itself

The crisis at Oma Säästöpankki is not the sum of individual errors — it is the consequence of a structural problem that existed from the very beginning. We have now spent over two years following how the bank first concealed its actions, apparently with success. The question we will address in our next article concerns the role of Finanssivalvonta and why both Finanssivalvonta and the KRP have acted slowly — even by Finnish standards — and, according to our information, provided a clear opportunity for the destruction of critical evidence and subsequent cover-up.

Foundation ownership creates a legally "ownerless" structure in which real power is concentrated in the hands of a few foundation chairs.

The permanence of the nomination committee enables a situation in which the same individuals — including, in all likelihood, a married couple whose relationship has not been disclosed — decide the composition of the board year after year.

Dual roles of management in owner foundations blur the line between owners and executive management. A dismissed CEO still manages the owner's investments.

Overlapping roles of board members — such as Mäkynen's simultaneous membership on OmaSp's board and the Bank of Finland's Payment Council — create structural conflicts of interest.

The intertwining of subsidiary boards with bank management enables a situation in which the same individuals who make lending decisions are the ones who benefit from them.

Widespread employee share ownership binds the entire organisation to silence. When over 60 per cent of staff own shares in their employer, reporting misconduct is a self-harming financial act. The whistleblowing channel remained empty.

And ultimately, when documents vanish from vaults, no one asks too many questions — because everyone has something to lose.

Open questions and forthcoming answers

This analysis does not provide all the answers. It raises questions that demand intensive investigation:

On the documentation: Who exactly had access to the vault? When did documents disappear? Is the disappearance random or systematic?

On the nomination committee: Why has the Lamminmäki couple's relationship not been disclosed? How has their conflict of interest been handled?

On management roles: Why is Sydänlammi permitted to continue as agent of an owner foundation? Who made that decision?

On oversight: Why did Finanssivalvonta's 2022 warnings not lead to action? Is the supervisory system structurally incapable of detecting problems when the supervised know the supervisors?

More broadly: Is the Finnish savings bank sector structurally susceptible to similar problems?

The investigation: According to our information, the KRP's investigation into many of these matters was still only "at the preliminary investigation stage" as of November 2025 — including with respect to Oma Säästöpankki. There are, of course, numerous investigative channels, but it is worth posing a final question: Who is standing over the KRP's investigation and has been actively steering it away from the bank? This is a matter to which we will certainly receive answers before long.

In closing: Trust must be earned — not only by OmaSp, but by the KRP, Finanssivalvonta, and the other safeguards

Raimo Härmä declared in the midst of the crisis: "Banking is a trust business."

He is right — but trust requires transparency. Transparency requires that power structures are clear and documented. That conflicts of interest are identified and reported. That oversight is real, not performative. And that documents remain in vaults rather than vanishing from them.

The case of Oma Säästöpankki shows what happens when these basic conditions fail. When a structure elects itself, it also oversees itself — and when no outsider asks questions, documents can disappear without anyone noticing or caring.

The question is: who will ultimately be held accountable?

An educated guess: when the bank collapses, the taxpayers.

17 December 2025

Sources

Regulatory sources

Finanssivalvonta: Inspection reports 2022–2025, stock exchange announcements.

Patentti- ja rekisterihallitus (PRH): Foundation register, trade register, beneficial owner filings.

Keskusrikospoliisi: Pre-trial investigation notices 2024–2025.

Company documents

Oma Säästöpankki Oyj: Annual reports 2018–2024, stock exchange releases, Corporate Governance reports, nomination committee rules of procedure.

News sources

Talouselämä (Taneli Koponen): OmaSp article series 2024–2025.

Ilkka-Pohjalainen: Sydänlammi and Lamminmäki roles.

Yle: Finanssivalvonta investigation, insider trading charges.

Kauppalehti: Financial data and board changes.

Business records

Finder.fi, Proff.fi, Asiakastieto.fi: Personal and corporate registry data.

Other sources

Ylä-Satakunta: A. Lamminmäki Oy business acquisition 2023.

Bank of Finland website: Payment Council composition and mandate.

Whistleblowers in various organisations.